Before Covid-19, air transportation in Europe: an already fragile sector

Updated version

Glossary of the main terms used

Introduction

A fragmented intra-european market before the crisis

Air transport, a low-margin sector

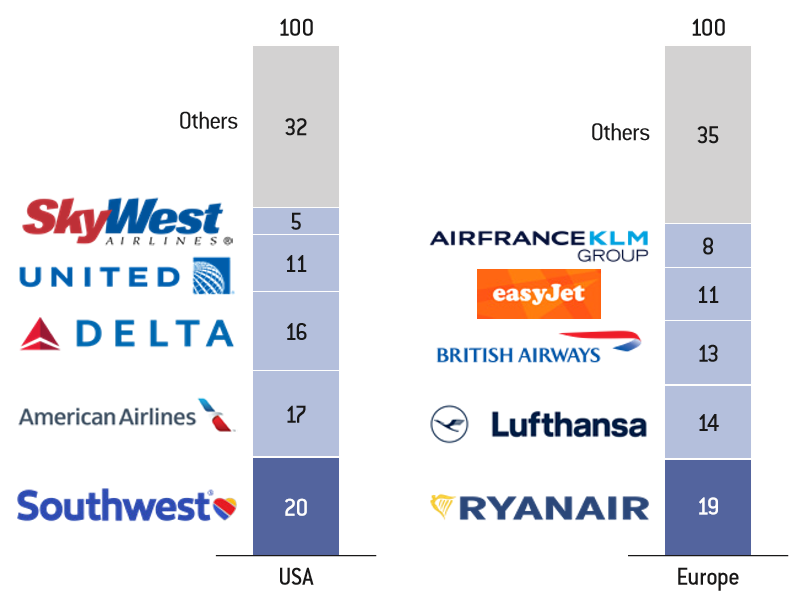

A European market less concentrated than in the United States

Numerous small actors

Covid-19 shock : historic companies in turmoil

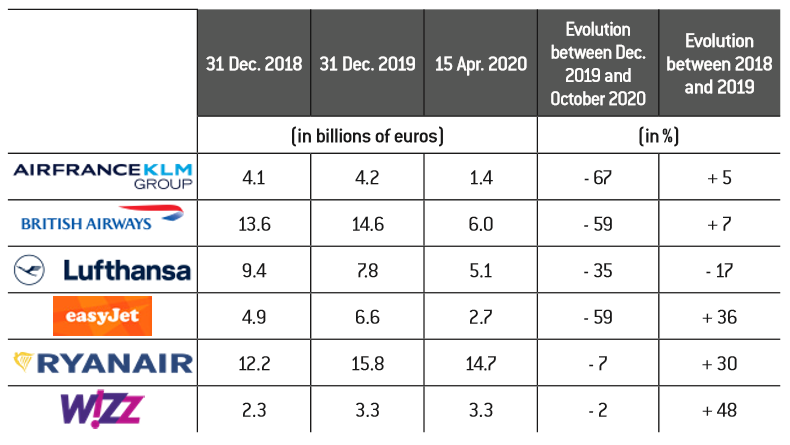

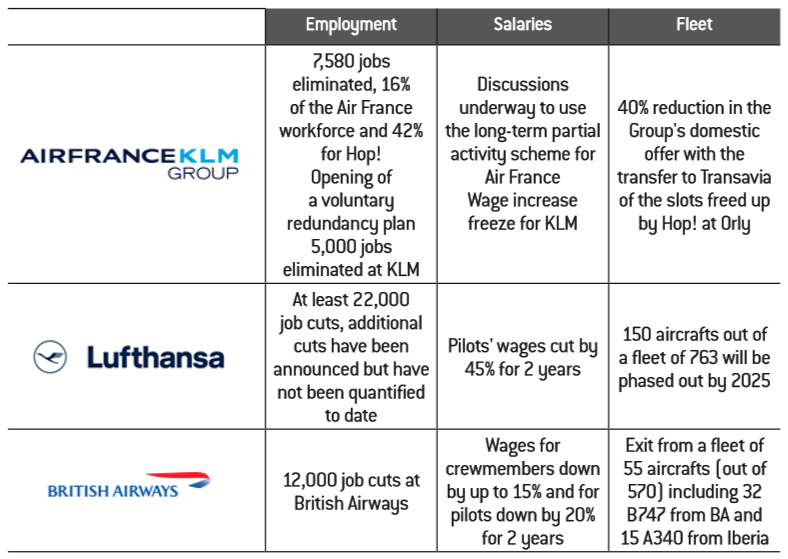

Two giants in turmoil: Air France-KLM and Lufthansa

An unavoidable call for public assistance

Covid-19 shock : the resilience of the low-cost giants

The ultra low-cost will survive the crisis

Middle-costs in a more critical situation

It is not enough to be big and low-cost: the Norwegian counterexample

Conclusion of the first volume

After Covid-19, air transportation in Europe: time for decision-making

Europe in the face of American and Chinese economic nationalisms (1)

Europe in the face of American and Chinese economic nationalisms (2)

Europe in the face of American and Chinese economic nationalisms (3)

Towards personalised pricing in the digital era ?

European airline rankings by financial strength

Copyright :

© Fondation pour l’innovation politique – 2020

Source :

Roland Berger.

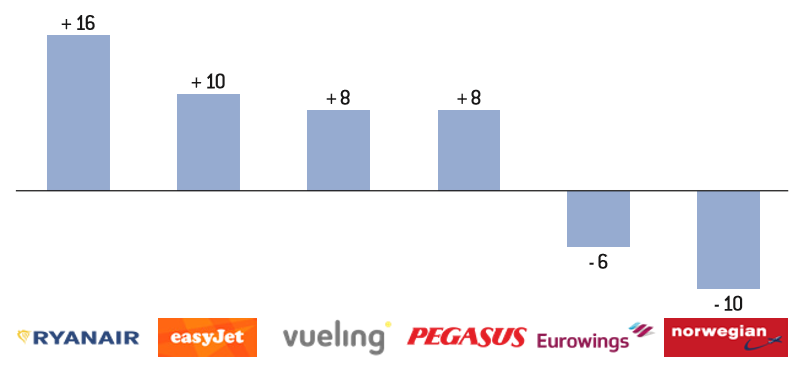

Evolution of market capitalisation during the Covid-19 crisis

Copyright :

© Fondation pour l’innovation politique – 2020

Source :

Roland Berger.

Share of intra-Europe/intra-US traffic by actors in 2019 (in %)

Copyright :

© Fondation pour l’innovation politique – 2020

Source :

Roland Berger, Bureau of Transportation Statistics, Innovata.

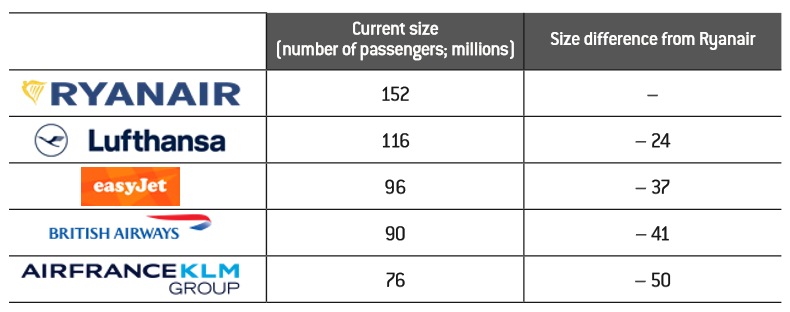

Number of passengers carried by the European leaders in the medium-haul market

Copyright :

© Fondation pour l’innovation politique – 2020

Source :

Roland Berger, based on airline company data.

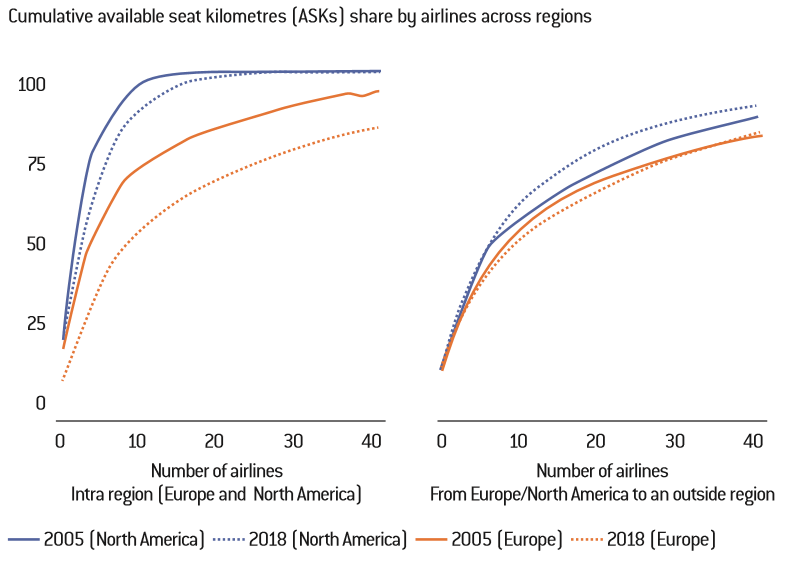

Airline consolidation compared between Europe and the U.S.

Copyright :

© Fondation pour l’innovation politique – 2020

Source :

PlaneStats.com; Airline schedule data, IATA industry statistics.

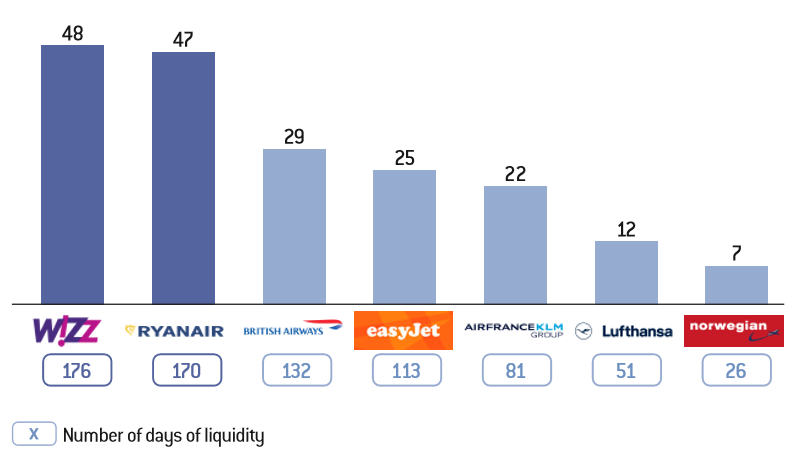

Share of cash to revenue and number of days equivalent in 2019 at the beginning of the crisis (in %)

Copyright :

© Fondation pour l’innovation politique – 2020

Source :

Roland Berger, CAPA, Company data.

Number of passengers carried by the European leaders in the medium-haul market

Copyright :

© Fondation pour l’innovation politique – 2020

Source :

Roland Berger.

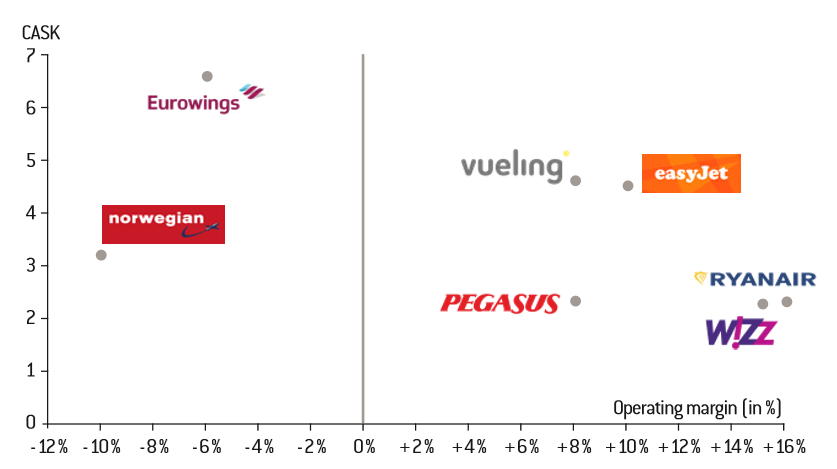

Operating margin for a sample of low-cost companies in 2018 (in %)

Copyright :

© Fondation pour l’innovation politique – 2020

Source :

Roland Berger, company data.

Unit cost per seat kilometre cents in euros in 2018

Copyright :

© Fondation pour l’innovation politique – 2020

Source :

Roland Berger, company data.